26 Aug Monthly Commentary: June 2022

Global equities – stabilisation as bond yields level out

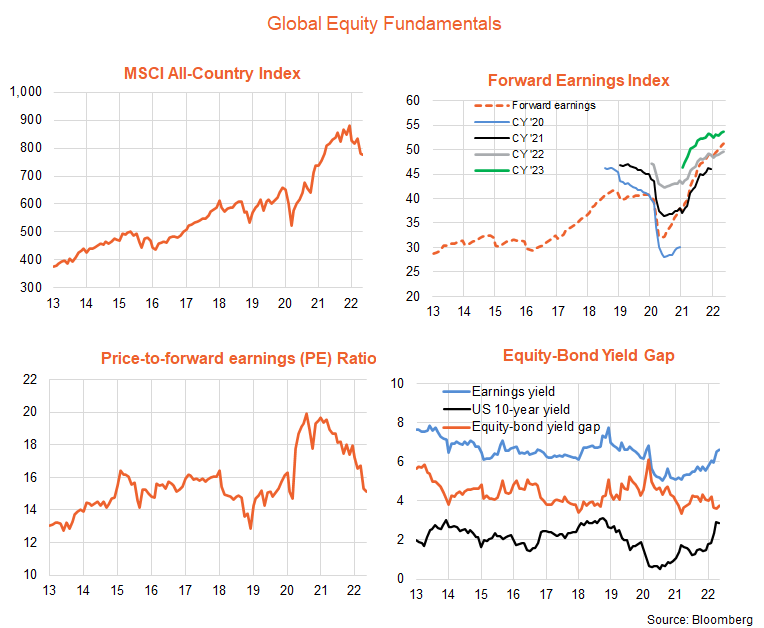

Global equities continued to weaken in May, albeit with a smaller drop than evident in April – helped by tentative signs that the lift in global inflation and bonds yields may be near a peak.

The MSCI All Country return index declined by 0.2% in local currency terms after a decline of 6.5% in April. Reflecting a firmer Australian dollar, the decline in unhedged global equities was a little greater at 1.4%, following a decline of 2.5% in April.

Forward earnings continued to grow, rising by 0.9% in the month with current market expectations consistent with further growth of 4.6% by end-22 and 7.5% over 2023. Accordingly, it was the PE ratio that again drove equity prices lower, falling from 15.3 to 15.1 – to be now broadly back in the range of the pre-COVID period since 2013.

Helping support risk sentiment was a stabilisation in bond yields, with the yield on U.S. 10-year bonds easing from 2.94% to 2.85%. In turn, this reflects a stabilisation in the market’s one-year ahead U.S. Fed funds rate hike expectation at around 3%.

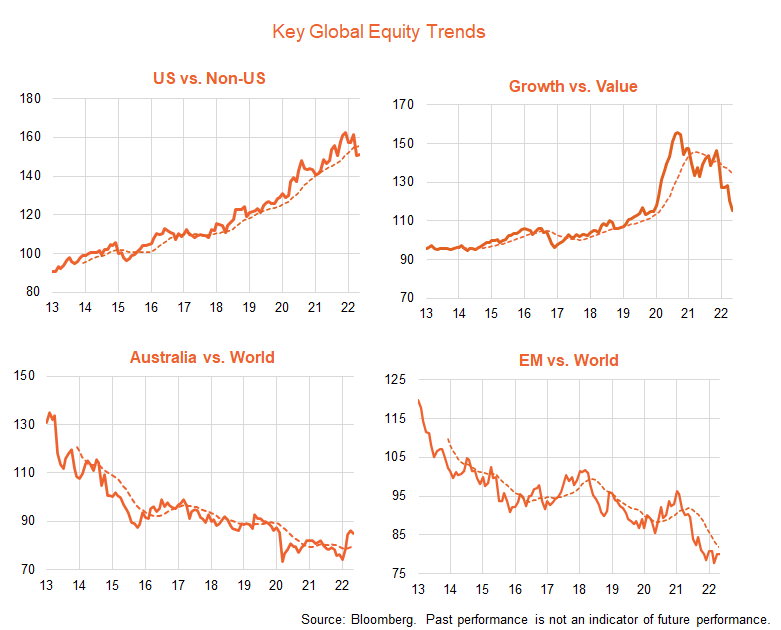

In a counter to recent trends, U.S. stocks did a little better than non-U.S. global stocks last month, though Australian stocks fared a little worse, even though growth stocks overall continued to underperform value stocks.

In terms of broad trends, the relative performance of the U.S. market appears to be weakening more clearly, in line with under-performance of growth versus value. Helped by stronger oil prices, the global energy sector was the strongest performer last month with a gain of 10.8%. Technology stocks declined by 1.1% after an 11.0% decline in April.

Global equity trends

Reflecting commodity price gains associated with the Russian invasion of Ukraine, commodity-related exposures such as energy and food retain the strongest relative performance trends among hedged global equity ETFs. Japanese stocks – helped by Yen weakness – are also displaying relative strength.

Among unhedged exposures, more defensive exposures such as UK stocks and global income continued to hold up better, with weakness still broadly evident among the technology thematics.

Australian equity trends

Local resource stocks bounced back modestly in May after a setback in April, and retain the strongest relative performance trend among key Australian equity ETF exposures. Local technology stocks remain under downward pressure, while more value type exposures such as financials and our fundamentally weighted Australian equity ETF have continued to hold up reasonably well.

This article was originally produced by David Bassanese from BetaShares you can read the full article here.

Next Steps

To find out more about how a financial adviser can help, speak to us to get you moving in the right direction.

Important information and disclaimer

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide.

FinPeak Advisers ABN 20 412 206 738 is a Corporate Authorised Representative No. 1249766 of Spark Advisers Australia Pty Ltd ABN 34 122 486 935 AFSL No. 458254 (a subsidiary of Spark FG ABN 15 621 553 786)

No Comments