26 Aug Monthly Commentary: July 2022

Global Equity Fundamentals – valuations OK, but earnings now a risk

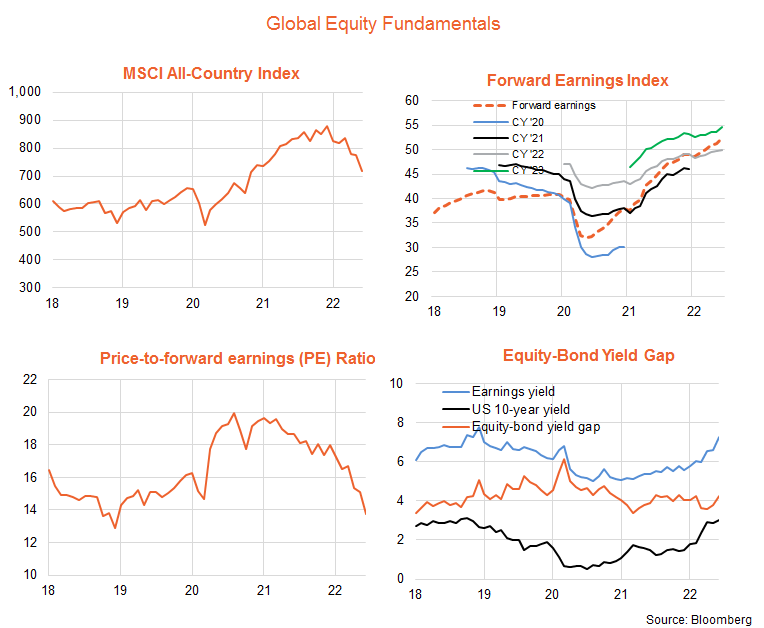

After some consolidation in May, global equities weakened further in June. The MSCI All Country World Index declined by 7.4% in local currency terms, after a decline of only 0.2% in May. The trend remains firmly down.

Helping drive prices lower was a rebound in bond yields, which had stabilised somewhat in May. US 10-year government bond yields rose by 17 basis points (bps) to 3.02%, after declining 9 bps in May. A stronger than expected US CPI report goaded the US Federal Reserve into raising rates by an aggressive 75 bps at the June policy meeting.

Combined with a rise in the equity risk premium of 50 bps to 4.26%, the market’s forward earnings yield rose 67 bps to 7.3% – implying a decline in the forward price-to-earnings ratio of 9.1% to 13.8 from 15.1.

The market’s PE ratio is now below its average of 15.6 since 2013. But given US 10-year bonds yields, at 3%, are above their average of 2% over this period, the market is only in line with its average equity risk premium of 4.4%.

Forward earnings continued to grow, rising by 1.7% in the month with current market expectations consistent with further growth of 4.5% by end-22 and 7.3% over 2023. There has yet to be a material downgrade to global earnings expectations, despite rising interest rates and fears of slowing growth.

The outlook remains vulnerable. I don’t believe US inflation will slow enough to allow the Fed to pause its aggressive rate hike campaign anytime soon. If we base recession on the Australian definition of two successive quarters of negative economic growth, the US already appears to have entered recession in the first half of this year. Q1 GDP growth was negative, and partial data suggests it remained negative in Q2.

If US recession does take root, it is likely that still-bullish earnings expectations will be revised down sharply and the PE ratio may also sink lower. One upside could be that bond yields stop rising, and may even fall. This will depend on how quickly weak economic growth causes inflation to slow, which would allow central banks to pause and potentially reverse their rate hike plans.

At some point, equity markets will also try hard to look through economic weakness and focus on economic recovery. But with still very tight labour markets, we’re likely to need more pain and spare capacity to be produced before we can focus on the upside.

Global Equity Themes – defensives and China

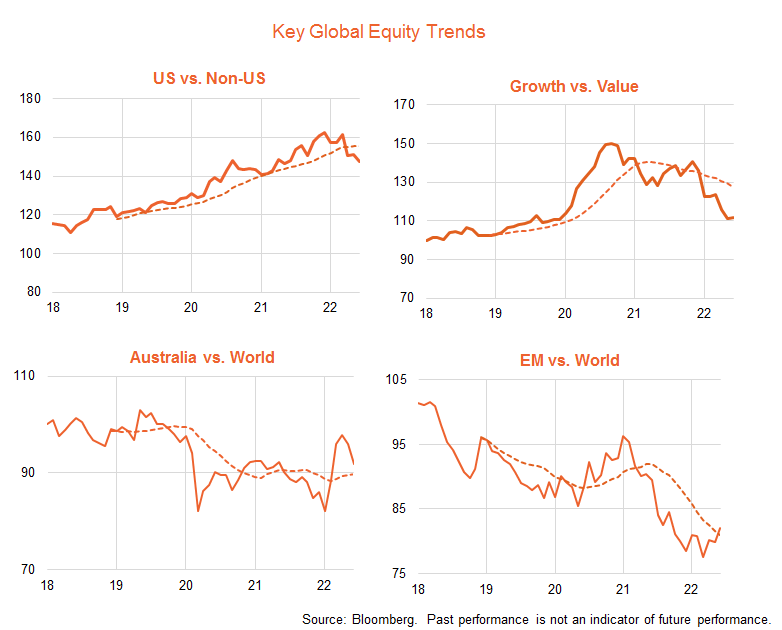

The trend of relative US underperformance reasserted itself in June, even though value sectors such as energy and financials performed almost as poorly as growth and technology stocks.

The theme of the month was a broadening in sector weakness beyond energy, commodity and financials stocks. Meanwhile, concerns about economic growth rose to compete alongside concerns over inflation and interest rates. This has also been reflected in catch-up weakness in the once-resilient local equity market.

The two sectors that held up best were the relatively defensive health care and consumer staples.

One other emerging trend is the relative strength in Chinese stocks, with the economy recovering from COVID-lockdowns and an easing in the harsh regulatory approach taken to leading technology companies. This has filtered through to an improvement in the relative performance of emerging markets in recent months.

Global equity trends

Among currency hedged global exposures, in a major counter-trend move, the former market darlings, global energy and food producers were the weakest performers in June, followed by global gold miners and banks. Those that held up best were Japanese equities – likely reflecting emerging optimism with regard to China – and the relatively defensive health care sector.

Among unhedged exposures, Asian technology held up best last month for reasons outlined above, while cyber security had a relatively small decline. Global income also held up relatively well, retaining its top performance rank. This reflected its more defensive qualities – a higher exposure to utilities and infrastructure.

The more value-biased exposures, UK stocks and the S&P 500 Equal Weight had a weaker performance in June, though retain their 2nd and 3rd longer-term relative performance ranking.

Australian Trends

Local resource stocks suffered a setback in April but retain the strongest relative performance trend among key Australian equity ETF exposures. Local technology stocks dropped in line with the global technology sell-off last month and retain the weakest relative performance trend. Australian financials continue to hold up reasonably well, and are performing notably better than their global counterparts.

This article was originally produced by David Bassanese from BetaShares you can read the full article here.

Next Steps

To find out more about how a financial adviser can help, speak to us to get you moving in the right direction.

Important information and disclaimer

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide.

FinPeak Advisers ABN 20 412 206 738 is a Corporate Authorised Representative No. 1249766 of Spark Advisers Australia Pty Ltd ABN 34 122 486 935 AFSL No. 458254 (a subsidiary of Spark FG ABN 15 621 553 786)

No Comments