Outlook for 2026 and Beyond: What We’ve Learned and What Matters Next

As we reflect on 2026, one thing is clear: this has not been a “normal” market cycle. Instead, it has been shaped by a small number of powerful forces that have dominated returns, challenged traditional diversification, and forced investors to make more deliberate choices.

Understanding these forces – and how they may shape the years ahead – is critical for long-term investors.

Looking Back: Markets in 2026

Despite periods of volatility, global equity markets proved more resilient than many expected. The early-year pullbacks tied to trade tensions and policy uncertainty were short-lived, with markets rebounding strongly as economic growth held up and earnings – particularly in the U.S. – remained robust.

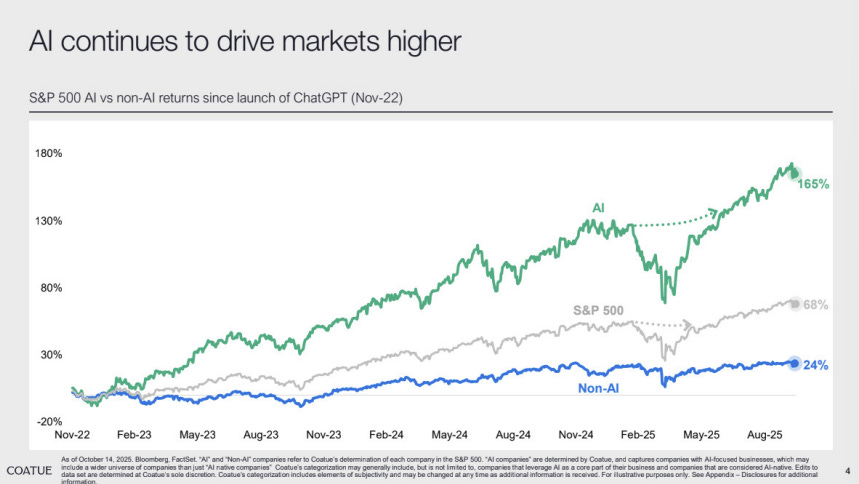

A defining feature of 2026 was market concentration. Returns were driven by a relatively narrow group of companies, largely tied to artificial intelligence (AI), infrastructure and energy. This meant that “the market” did well, but not all parts of the market moved together.

At the same time, bonds behaved differently to what many investors had grown used to. Long-term government bond yields remained under pressure due to rising government debt and fiscal concerns, even as central banks began easing policy. This challenged the traditional role of bonds as a reliable shock absorber in portfolios.

What Are Capital Market Assumptions – and Why They Matter

Capital market assumptions are long-term estimates of expected returns, risks and correlations across asset classes. They don’t predict what markets will do next year, but they help guide portfolio construction over the next 10 years and beyond.

BlackRock’s latest capital market assumptions reflect a world that looks very different from the past decade:

- Higher structural inflation than pre-COVID

- A higher cost of capital

- Greater dispersion between winners and losers

- More opportunity – and need – for active decision-making

In other words, broad, passive exposure alone may no longer deliver the same outcomes it once did. Investors may need to be more selective about where they take risk and how they diversify.

You can read further here.

BlackRock’s AI View: Opportunity, Not Autopilot

AI has been the dominant investment theme of this cycle – and BlackRock believes it is still in its early innings. Unlike past technology waves, AI is capital-intensive, requiring enormous upfront investment in data centres, chips, power generation and infrastructure.

BlackRock estimates that global AI-related capital spending could reach US$5–8 trillion by 2030. That scale of investment is unprecedented and has real economic consequences, influencing growth, inflation, energy demand and capital markets more broadly.

However, this does not mean every AI-related company will be a winner. A key question is who ultimately captures the revenues created by AI. This is why BlackRock sees AI less as a passive “buy everything” story and more as an active investment opportunity, where selectivity will matter more over time.

Importantly, BlackRock believes that if AI meaningfully lifts productivity, it could help economies grow faster than their long-term trend – something that has not happened after previous technological revolutions. While not guaranteed, it is now conceivable for the first time in decades.

Key Themes from the 2026 Global Outlook

BlackRock’s 2026 Global Outlook, titled “Pushing limits”, highlights three powerful ideas that investors should keep in mind:

1. “Micro is macro”

The investment decisions of a small number of very large companies – particularly in AI – are now big enough to influence the entire economy. This blurs the line between company-level analysis and macroeconomic outcomes.

2. A more leveraged system

AI investment is front-loaded, while revenues come later. This has led to increased borrowing by companies at a time when governments are already heavily indebted. The result is a system that may be more sensitive to interest rates and bond market volatility.

3. The diversification mirage

What looks like diversification on the surface may actually be a large active bet underneath. For example, moving away from U.S. equities or AI-exposed assets may reduce exposure to the very forces driving returns – without necessarily reducing risk.

Because of this, BlackRock emphasises scenario-based investing, private markets, and more granular portfolio construction rather than relying solely on traditional asset class labels.

What This Means for Investors

The key takeaway from 2026 is not that markets are “too expensive” or that a downturn is imminent. Rather, it’s that the investment environment has changed.

Markets are being driven by a small number of structural forces – especially AI – and investors can no longer avoid making meaningful decisions about them. The challenge, and opportunity, lies in building portfolios that are resilient across different scenarios while remaining positioned for long-term growth.

As always, the focus should remain on:

- Staying diversified, but deliberately so

- Looking beyond short-term noise

- Aligning portfolios with long-term objectives, not headlines

If the last few years have taught us anything, it’s that adapting thoughtfully matters far more than trying to predict the next twist in markets.

Next Steps

To find out more about how a financial adviser can help, speak to us to get you moving in the right direction.

Important information and disclaimer

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide.

FinPeak Advisers ABN 20 412 206 738 is a Corporate Authorised Representative No. 1249766 of Spark Advisers Australia Pty Ltd ABN 34 122 486 935 AFSL No. 458254 (a subsidiary of Spark FG ABN 15 621 553 786)