Market Trends May: Debt Ceiling Concerns

Market Summary

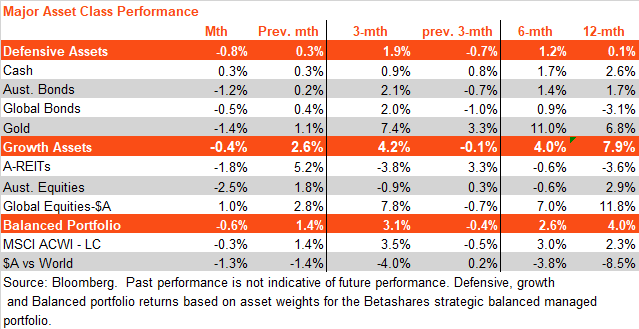

Growth and defensive asset returns were modestly negative in May as rising bond yields and concerns over a potential US debt default weighed on sentiment – while earlier fears of a US banking crisis continued to wane.

An easing in US bank concerns has returned investor focus to the resilience of US economic growth and inflation and the potential need for the US Federal Reserve to increase policy rates further.

A faltering in China’s pace of economic recovery following the end of COVID-related restrictions also dented investor enthusiasm, especially in commodity-related markets such as Australia. The lingering risk of higher local interest rates from the Reserve Bank of Australia also weighed on local bond and equity returns.

Fixed-rate bonds

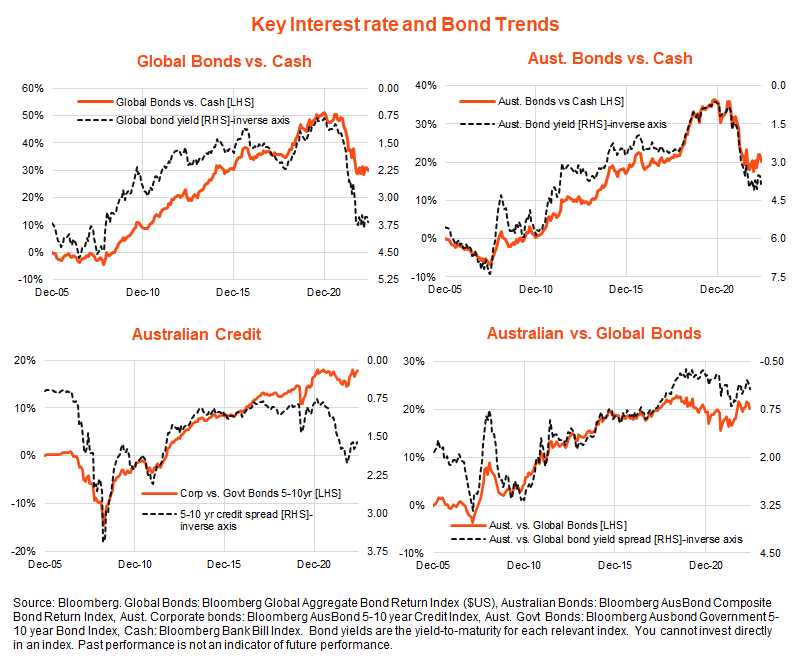

A bounce back in bond yields hurt fixed-rate bond returns in May. The yield on US 10-year government bond yields rose by 0.22% to 3.65%, after declining in April. The US market ended the month expecting one further 0.25% Fed rate rise over the coming months and no rate cuts until early next year. The Bloomberg Global Aggregate Bond Index ($A hedged) declined by 0.5% in May after a 0.4% gain in April.Australian 10-year bond yields rose by 0.27% to 3.61% over the month, with the market pricing in one further rate hike this year. The Bloomberg AusBond Composite Index declined by 1.2% in the month after a 0.2% gain in April.

As evident in the chart set below, long-term bond yields appear to be topping out as central bank tightening cycles draw to a close. This has seen the performance of bonds relative to cash improve since late last year.

Credit spreads have also narrowed with the recovery in equity prices from late last year. Australian bonds have tended to outperform global bonds, given the relatively less aggressive rate hikes expected from the RBA.

Gold

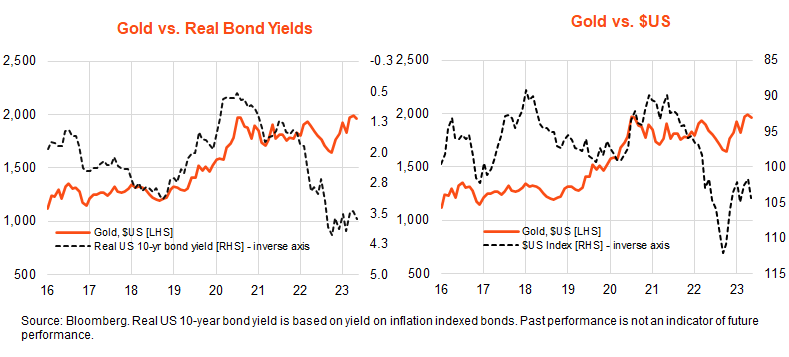

Gold prices eased back 1.4% in May, after a 1.1% gain in April, likely reflecting the rise in both bond yields and the US dollar. As was the case early last year, a potentially more aggressive Federal Reserve would likely be adverse for gold prices over the near term, though an eventual further easing in bond yields and the US dollar would be positive forces.

Global equities

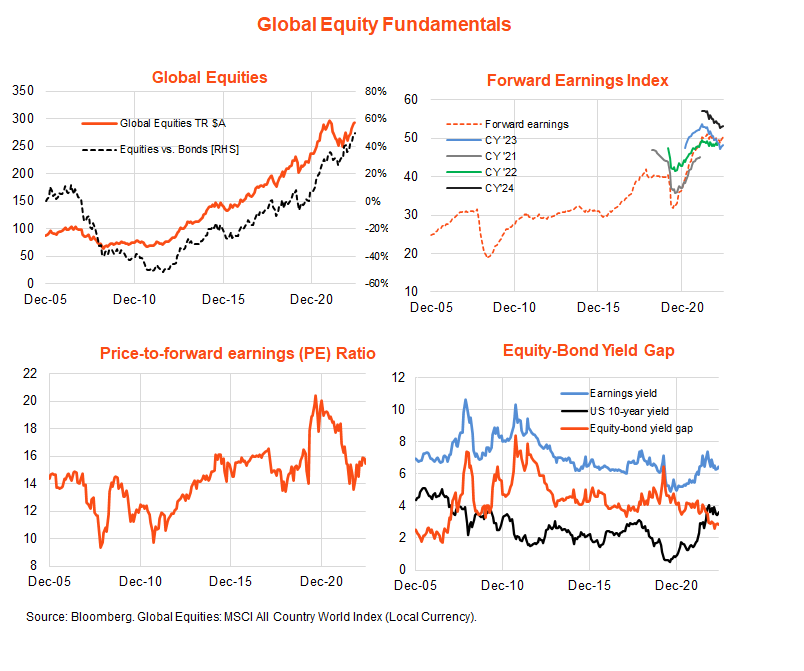

Global equities eased back 0.3% in local currency terms in May as modest growth in forward earnings was more than offset by a decline in PE valuations as bond yields rose. In $A terms, global equities returned a positive 1.0% reflecting weakness in the $A.

The upturn in forward earnings, after declines over recent months, is notable and points to still fairly resilient global economic growth in the face of central bank tightening.

Despite recent earnings declines, global equities have generally performed better than global bonds since around mid-2022. That said, much of this outperformance has reflected a decline in the equity risk premium to below 3% compared with an average of just over 4% since the mid-2000s.

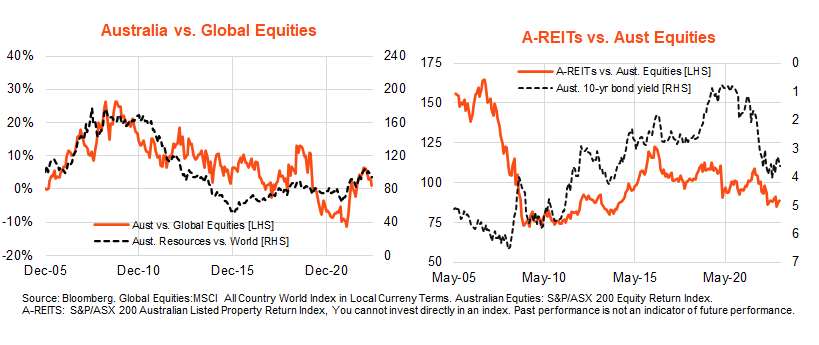

Australian equities and listed property

Australian equities declined by 2.5% over May, underperforming global equities, reflecting weakness in resource and consumer stocks and a relatively small weighting to the strongly performing technology sector. Australian equities have tended to underperform global equities in recent months due to the easing in bond yields and an associated improvement in sentiment towards growth over value stocks.

The volatility of listed property returns continued in May with a solid 1.8% decline after a solid 5.2% rise in April. Despite a general easing in bond yields since late last year, listed property performance has been muted, likely reflecting concerns over rising office vacancy rates and whether valuations have yet to fully reflect the rise in bond yields over the past year.

The volatility of listed property returns continued in May with a solid 1.8% decline after a solid 5.2% rise in April. Despite a general easing in bond yields since late last year, listed property performance has been muted, likely reflecting concerns over rising office vacancy rates and whether valuations have yet to fully reflect the rise in bond yields over the past year.

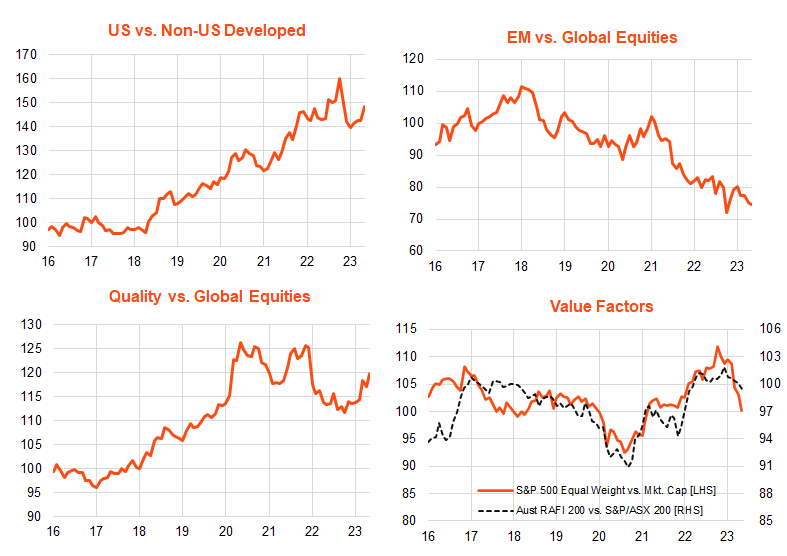

Global equity themes

Despite the lift in bond yields in May, technology/growth/US market themes continued to outperform commodity/value/non-US exposures over the month, likely helped by growing investor enthusiasm for artificial intelligence.

By factor, the relative performance of global quality has also improved since late last year, while that of more value-oriented exposures has eased.

Source: Bloomberg. Indices: US: S&P 500. Non-US Developed: MSCI World, ex-US. Global Equities: MSCI ACWI. Emerging markets (EM): MSCI Emerging markets. Quality: iSTOXX MUTB Global Ex-Australia Quality Leaders Index AUD Hedged. Mkt. Cap: CRSP US Total Market Index. You cannot invest directly in an index. Past performance is not an indicator of future performance.

Outlook

Whether or not the US economy can pull off a soft landing remains the critical driver of global market trends. Prior to the recent increase in global banking instability, renewed fears of an overly strong US economy were beginning to outweigh hopes of a soft landing that had been in place since around October last year.

Easing bank fears has returned focus to America’s inflation challenge. Yet while US economic growth has so far remained stubbornly resilient, it’s also true that price and wage inflation pressures appear to be easing – with the latter helped by a decline in labour demand and a rebound in labour supply.

We remain in a state of flux. While some US indicators – such as weakness in manufacturing and very inverted yield curves – point to impending recession, underlying consumer spending and employment demand remain robust. And while price and wage inflation are easing, they also remain uncomfortably high.

My base case still errs towards stubbornly high US wage and price inflation and so an eventual US recession – caused by a tightening in lending conditions and/or aggressive further Fed rate hikes. Indeed, history suggests it should be hard to get US inflation sustainably lower without a material weakening in the still very tight labour market.

The resilience of the US economy and the degree of monetary tightening required to get this hard landing, however, will determine whether we need to go through a ‘no landing’ scenario before we get there.

This article was originally produced by David Bassanese from BetaShares. You can read the full article here.

Next Steps

To find out more about how a financial adviser can help, speak to us to get you moving in the right direction.

Important information and disclaimer

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide.

FinPeak Advisers ABN 20 412 206 738 is a Corporate Authorised Representative No. 1249766 of Spark Advisers Australia Pty Ltd ABN 34 122 486 935 AFSL No. 458254 (a subsidiary of Spark FG ABN 15 621 553 786)