Home Loans in 2024: Trends, Tips, and How to Make the Most of Your Mortgage

Navigating the 2024 home loan landscape requires a clear understanding of evolving trends and smart strategies. With interest rates stabilising yet remaining high and borrowing capacity influenced by strict serviceability requirements, borrowers face unique challenges. Despite these pressures, steady property price growth signals opportunities for savvy buyers. This article explores key trends and practical tips to help you optimise your mortgage and make the most of the current market.Average loan sizes and how to pay off faster

The average Australian homeowner is borrowing $636,209 for a home loan, with loan amounts varying significantly across states, according to data from the Australian Bureau of Statistics. The table below provides a breakdown of the figures:

Whether your loan amount is above or below these averages, reducing your mortgage balance is likely a key priority. Here are some strategies to help you achieve that:

- Switch to fortnightly repayments: This simple change adds an extra month's worth of repayments each year.

- Utilize offset or redraw facilities: If available, these features can help lower your interest charges.

- Refinance to a lower interest rate: Competitive deals are often available for borrowers with at least 20% equity.

Each of these approaches depends on your unique financial situation. Feel free to get in touch if you’d like assistance in exploring your options or running the numbers.

Lenders competing strongly for borrowers

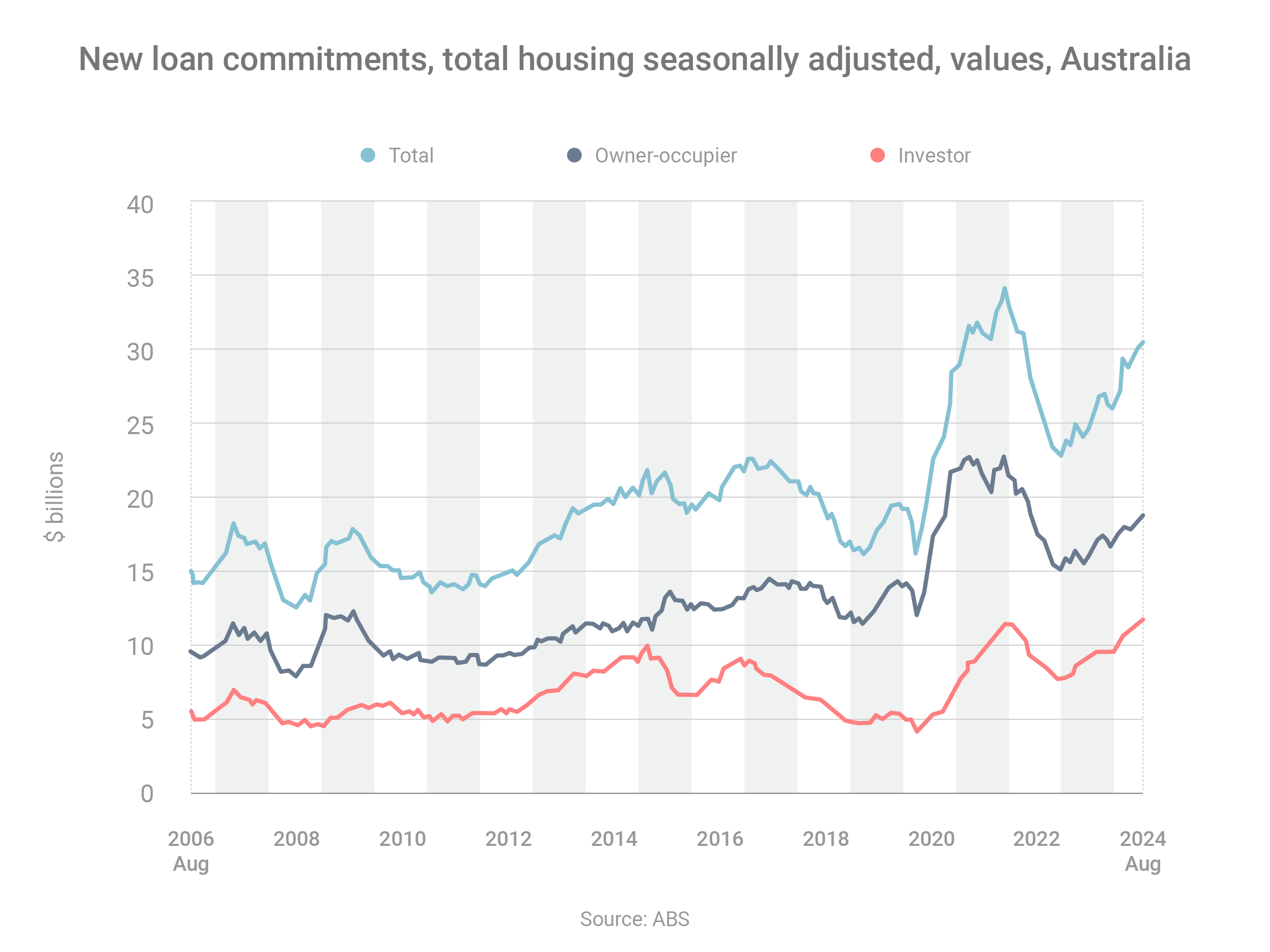

Lenders are fiercely competing for borrowers, especially those with strong credit profiles. This competition has driven borrowing activity up by 18.2% between January and August 2024, according to the latest data from the Australian Bureau of Statistics.

During this period, owner-occupier borrowing increased by 14.9%, investor borrowing surged by 23.7%, and refinancing activity saw a modest rise of 1.2%.

If you haven’t reviewed your existing loan in the past two years, now might be the perfect time to explore better options. Or, if you’re planning to buy, let’s discuss how I can assist you.

Here’s how I can help:

- Compare loans from a wide range of lenders to find the best fit.

- Maximise your borrowing capacity to suit your financial goals.

- Tailor a strategy and loan structure that aligns with your unique circumstances.

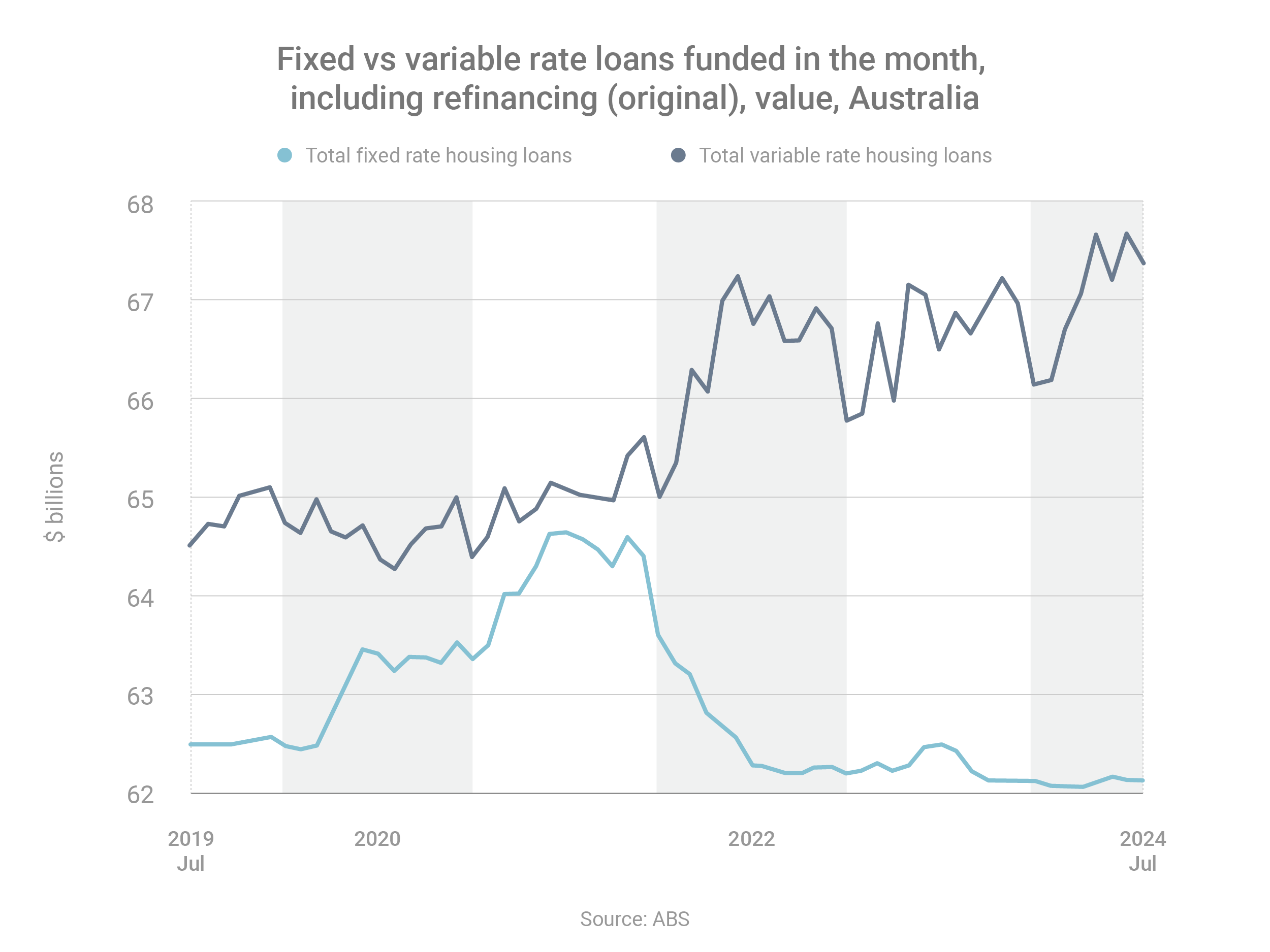

Why 98% of borrowers are going variable right now

Most home loan borrowers are currently favoring variable-rate loans over fixed-rate options.

In August 2024, 98% of new loans were variable, while just 2% were fixed, according to the latest data from the Australian Bureau of Statistics.

This marks a significant shift from August 2021, when interest rates were at record lows. Back then, 46% of borrowers opted for fixed-rate loans, while 54% chose variable.

Borrowers’ decisions appear to be driven by their expectations of future interest rate movements:

- In 2021, with rates at pandemic-driven lows, many borrowers expected rate hikes and locked in the lower rates with fixed loans.

- In 2024, most borrowers believe rates have peaked, so they’re choosing variable loans, anticipating potential rate cuts by the Reserve Bank of Australia.

Fixed vs. Variable Loans

- Fixed loans: These provide repayment certainty, as your monthly payments stay the same during the fixed period. While this protects you from rising rates, you won’t benefit if rates fall.

- Variable loans: These are less predictable, as repayments fluctuate with interest rate changes. They increase when rates rise but decrease when rates fall.

Choosing between fixed and variable depends on your financial goals and risk tolerance. If you’re unsure which is right for you, feel free to reach out for tailored advice.

This article was originally produced by Dawn Inanli from FinPeak Finance.

Next Steps

To find out more about how a financial adviser can help, speak to us to get you moving in the right direction.

Important information and disclaimer

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide.

FinPeak Advisers ABN 20 412 206 738 is a Corporate Authorised Representative No. 1249766 of Spark Advisers Australia Pty Ltd ABN 34 122 486 935 AFSL No. 458254 (a subsidiary of Spark FG ABN 15 621 553 786)