Gold as an Investment: Why It Still Matters in a Diversified Portfolio (with Recent Performance)

Gold is not just theoretical insurance — recent data shows how it has behaved relative to equities and bonds over the past decade. Below is a comparison, followed by an updated discussion of what that means for portfolio construction.

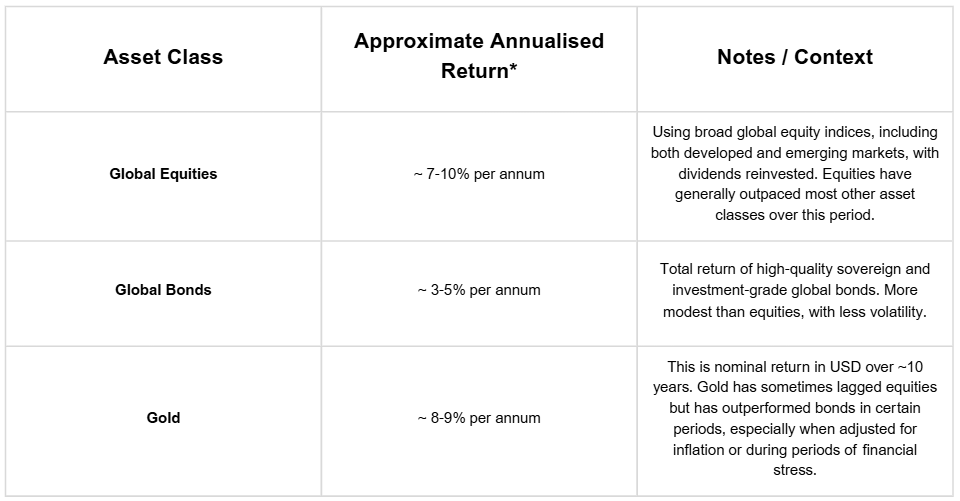

Recent 10-Year Performance Snapshot

These are approximate, nominal returns (i.e. before inflation), and for illustrative purposes only. Different sources/currencies/indexes give somewhat different results.

Here are some more detailed data points:

- According to UpMyInterest, gold’s mean annual return over the last 10 years has been about 8.8% per year.

- Damodaran / “A Wealth of Common Sense” reports global long-term averages (stocks vs bonds vs gold etc.), but over shorter recent windows equities have clearly led, as per multiple datasets.

- Gold’s annual returns year by year have been quite volatile; years of strong returns (e.g. ~25-30%) have alternated with flat or negative years. For example, in some recent years gold’s USD return was in the high 20s, while other years saw small losses.

What the Data Tells Us: Implications for a Portfolio

Using that performance data, here's how gold fits into a diversified portfolio, particularly relative to equities and bonds:

-

Equities tend to lead in growth over long periods, especially when economic conditions are reasonably stable, corporate earnings grow, and interest rates are moderate. Over the past ~10 years, equities have generally delivered higher returns than bonds and often higher than gold (though in certain years gold has done very well).

-

Bonds provide stability, income, and lower volatility. Their returns are smoother, but lower on average. When equities decline or bond yields behave favourably (or when real yields are low or negative), gold often steps up, helping cushion downside risk.

-

Gold’s role as a hedge is validated by its returns in specific stress periods, inflationary periods, and times when bond markets are under pressure. While its average return over 10 years isn’t always the highest, its risk-adjusted contribution and low correlation with the worst years of equities or bonds can be valuable.

-

Inflation and real return matters: When inflation is high (or rising), and/or when real interest rates (interest minus inflation) are low or negative, gold tends to perform relatively well. Bonds then often suffer in real terms, especially longer-duration ones.

-

Volatility vs. reward trade-off: Gold can be volatile. It doesn’t pay dividends or coupons. Because of that, there’s an opportunity cost in holding gold when equities are booming. But that cost may be worth it for insurance benefits — reducing drawdowns, providing portfolio insurance, etc.

Gold has long held a unique place in financial markets. Unlike equities or bonds, it doesn’t generate income, yet it has been trusted for centuries as a store of value. Today, gold continues to play a role in modern investment portfolios — not for what it earns, but for how it behaves when other parts of the market come under pressure.

A Historical Store of Value & Recent Returns

Gold has been recognised as a currency and store of wealth across cultures for thousands of years. While modern economies no longer use the gold standard, investors continue to turn to it during periods of uncertainty.

Over the past 10 years, gold has delivered nominal annualised returns in the order of 8-9% in US Dollars. In certain years, returns were exceptionally strong (20-30%), while in others, gold’s returns were flat or even modestly negative. This contrasts with global equities, which have delivered somewhat higher average returns over the same period (around 7-10%, depending on region and index), but with risk of larger drawdowns. Global bonds, on the other hand, have produced lower returns (roughly 3-5% per annum), with smoother trajectories. (These numbers vary by source, currency, inflation etc.)

This recent performance underscores gold’s dual role: a vehicle for long-term value preservation and a buffer during market stress or inflationary regimes.

Portfolio Diversification and Risk Management

Gold’s real strength lies in diversification. It tends to move independently (or even inversely) of other major asset classes such as equities and bonds. When markets experience stress — particularly when US Treasury or global bond markets come under pressure — gold has historically provided ballast.

This has been visible in years recent where bond yields rose or real yields turned negative: traditional bond-based “defensive” allocations suffered, but gold often delivered positive returns (or at least weaker losses), helping to reduce overall portfolio drawdown.

Hedge Against Drawdowns & Inflation

During periods of high inflation, weakening currencies, elevated geopolitical risk, or fiscal/monetary policy shocks (e.g. rate hikes), gold has tended to outperform many fixed income instruments. Over the past decade, the relative performance of gold versus bonds improved in years when inflation spiked and nominal bond yields rose — but real yields fell or were negative.

Equities in those times have sometimes done poorly (or been volatile), so gold’s return profile during those periods makes it a useful hedge.

Limitations Revisited with Performance in Mind

- Gold doesn’t provide income (no dividends or coupons) — so when bonds are offering attractive real yields, gold may lag after opportunity cost is considered.

- Its volatility means that though the average return over 10 years is decent, some years hurt — which might test the resolve of investors if gold represents a significant portion of the portfolio.

- Definitely, when equities are booming (and especially tech/growth stocks), gold tends to lag in total return.

Final Thoughts: What This Means for Portfolio Construction

Given the recent performance:

- A modest allocation to gold (e.g. 5-10%) may help smooth returns, especially during times when equities or bonds suffer drawdowns.

- Gold is particularly valuable when real yields are low or negative, inflation is rising, or interest rate uncertainty is high.

- It should be viewed as part of the defensive or risk-mitigating portion of the portfolio, not the core growth engine.

- The precise allocation depends on your risk tolerance, investment horizon, whether you believe inflation or bond stress risks are elevated, and what your other portfolio exposures are.

Next Steps

To find out more about how a financial adviser can help, speak to us to get you moving in the right direction.

Important information and disclaimer

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide.

FinPeak Advisers ABN 20 412 206 738 is a Corporate Authorised Representative No. 1249766 of Spark Advisers Australia Pty Ltd ABN 34 122 486 935 AFSL No. 458254 (a subsidiary of Spark FG ABN 15 621 553 786)