On 6 October 2020, the Government handed down the 2020-21 Federal Budget with the Treasurer outlining the economic recovery plan for Australia by providing tax relief, encouraging job creation, rebuilding our economy and securing Australia’s future as the dominant themes.

Watch on YouTube — Watch on YouTube

Watch on YouTube — Watch on YouTube Overview

The COVID-19 pandemic has had a profound impact on Australia’s health system, community and economy. The Government has provided $257 billion in support to cushion the economic impact of COVID-19. In doing so, the Treasurer had the unenviable task of revealing the Budget deficit will increase to $213.7 billion this year.The focus of the 2020-21 Budget is the path to recovery with the plan focused on growing the economy so Australia can create jobs, increase economic resilience and create a more competitive and income generating economy.

From a pure financial planning and wealth perspective, the positive news from this year’s Budget is that the changes are minimal and largely positive in nature. From personal tax cuts from 1 July 2020, tax free payments for certain welfare recipient as well as some enhancements to the superannuation system, there is something for nearly everyone in this Budget. Of particular significance this year, there is no significant tinkering of our superannuation system. The rumoured changes to super guarantee arrangements has not eventuated, and there has been no further extension of the early access measure.

Below provides an overview of the measures announced in this years Federal Budget.

It is always important to remember that at this point, the Budget night announcements are only statements of intended change and are not yet law. A financial adviser can help outline what these measures may mean for you.

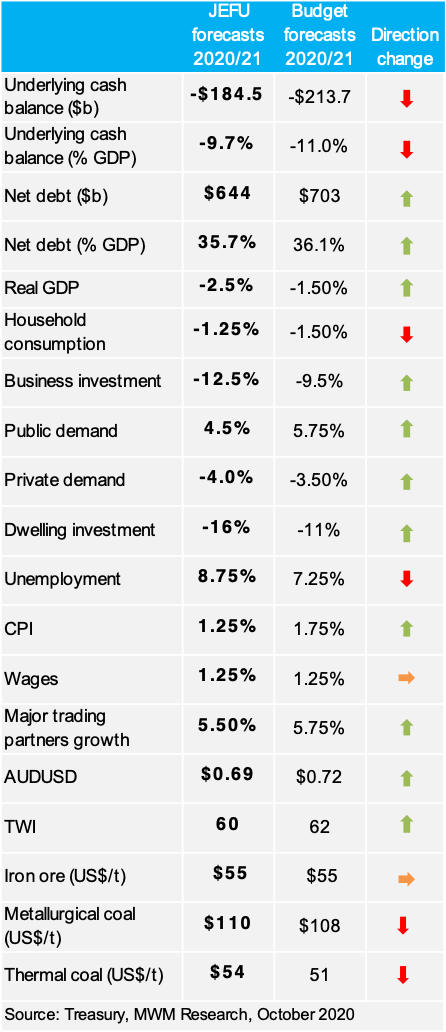

The table below highlights the key budget forecasts and changes since the July Economic and Fiscal Outlook (JEFU).

Key highlights:

- The delayed 2020/21 Federal budget is the most significant in decades. The aim is that it will go down in history as the budget that lifted Australia’s economy out of recession via a government-backed jobs recovery.

- The overriding thrust of the budget is about transitioning the economy off unsustainable welfare payments (JobKeeper) via a heavy emphasis on policies that support job creation (JobMaker).

- The budget shows a continuation of the willingness of government to support the economy through this transition. In combination with emergency monetary policy settings, the combination of expansionary fiscal policy provides an unparalleled level of policy stimulus for the Australian economy.

- Debt levels are set to increase significantly but this as unavoidable and a necessary response given the size of the economic hit and the ongoing headwinds that this has created.

- This is a very positive budget which should be greeted with enthusiasm despite the depth of the problems it seeks to address. The Government has shown a clear willingness to kick-start the recovery while putting aside concerns about soaring debt levels. We think this is the right approach and treads a line between balancing short versus long term objectives.

- We think investors should welcome this pro-growth budget which addresses ‘fiscal cliff’ concerns, pulls forward tax-cuts and looks to turbo-charge the recovery via job creation. In combination with record low borrowing rates and forward guidance provided by the RBA, we think policy makers have not lacked in their willingness nor the level of policy support to get the economy back to a self-sustaining level as quickly as possible.

Budget winners and losers:

Winners:

Low/Middle income earners – pull forward second stage of Personal Income Tax Plan, retain low and middle income tax offset (LAMITO).

Businesses – heavily incentivised to hire younger staff (JobMaker, apprenticeships), cash flow boost from instant asset write-offs and $2b for R&D Tax Incentive.

Property – expansion of the First Home Loan Deposit Scheme (FHLDS) and CGT relief for granny flats.

Infrastructure – $10b in funds available to the states, focus on ‘shovel-ready’ projects (roads, councils).

Source: Budget.gov.au, MWM Research, October 2020

Losers:

High income earners – tax relief remains long-dated (2024) with no pull forward as initially speculated.

Welfare – the transition away from JobKeeper will be difficult for those that may not have a job to return to when the program expires in March 2021.

Superannuation reforms – increased regulation for super sector with a greater focus on transparency, fees and underperforming funds. Expect ongoing industry consolidation.

Mega-caps – Businesses with annual turnover >$5b will miss out on support measures.

Source: Budget.gov.au, MWM Research, October 2020

This was an extraordinary budget for extraordinary times. The Australian economy has been on life-support since COVID-19 hit the global economy in 1Q20 but now needs a major kickstart to get going again. The Federal Government has successfully minimised the downturn and is now looking to maximise the upturn via a range of growth-positive initiatives we review below.

Personal Tax Cuts

Australian taxpayers are set to benefit immediately as the Government plans to bring forward the tax cuts in Stage 2 of the Personal Income Tax Plan from 1 July 2022 to 1 July 2020. Key highlights of this measure include the following:

– The top threshold of the 19% personal income tax bracket will increase from $37,000 to $45,000.

– The top threshold of the 32.5% personal income tax bracket will increase from $90,000 to $120,000.

– The Low Income Tax Offset (LITO) will increase from $445 to $700. The increased LITO will be withdrawn at a rate of 5 cents per dollar between taxable incomes of $37,500 and $45,000. The LITO will then be withdrawn at a rate of 1.5 cents per dollar between taxable incomes of $45,000 and $66,667.

– The Low And Middle Income Tax Offset (LMITO) will be retained for the 2020-21 financial year.

Importantly, the already legislated tax cuts will see 95 per cent of taxpayers face a marginal tax rate of no more than 30 cents in the dollar from 1 July 2024.

Additional payments for eligible social security recipients

Two separate $250 payments will be made to eligible Australians in receipt of certain income support payments including the age pension, carer payment and family tax benefits, and also health care cardholders. An individual maybe eligible to receive both $250 payments, however they can only receive one $250 per round even if they qualify per round in multiple ways.

The payments will be exempt from taxation and not count as income for Social Security purposes.

Your future, your super

This year’s Federal Budget has made enhancements to the super system to ensure your super is working harder for you. These are summarised below:

– From 1 July 2021, you will keep your super fund when you change jobs, stopping the creation of unintended multiple super accounts and the erosion of your super balance.

– Creation of the YourSuper comparison tool to help you decide which super product best meets your needs.

– By 1 July 2021, MySuper products will be subject to an annual performance test. If a fund is deemed to be underperforming, it will need to inform its members of its underperformance by 1 October 2021.

Importantly, the rumoured changes to super guarantee (SG) arrangements have not eventuated so this means that from 1 July 2021, the rate of SG will start its gradual half percent increase per annum from the current 9.5% up to 12% by 1 July 2025.

Temporary loss carry-back provisions for business with turnover less than $5 billion

To support business cash flow, eligible companies will be able to carry back tax losses from the 2019-20, 2020-21 or 2021-22 income years to offset previously taxed profits in 2018-19 or later income years.

Companies with an aggregated turnover of less than $5 billion can apply tax losses against taxed profits in the previous years noted, generating a refundable tax offset in the year in which the loss is made.

Temporary full expensing of eligible capital assets

Business with aggregated annual turnover of less than $5 billion will be able to deduct the full cost of eligible capital assets acquired from 7.30pm AEDT on 6 October 2020 (Budget night) and first used or installed by 30 June 2022.

Full expensing in the year of first use will apply to new depreciable assets and the cost of improvements to existing eligible assets.

Businesses with aggregated annual turnover of less than $50 million can also apply full expensing to second-hand assets.

Businesses with aggregated annual turnover between $50 million and $500 million can still deduct the full cost of eligible second-hand assets costing less than $150,000 that are purchased by 31 December 2020 under the enhanced instant asset write-off. These businesses will have an extra six months, until 30 June 2021, to first use or install those assets.

Businesses with aggregated annual turnover of less than $10 million can deduct the balance of their simplified depreciation pool at the end of the income year while full expensing applies. The provisions which prevent small businesses from re-entering the simplified depreciation regime for five years if they opt-out will continue to be suspended.

Qualifying business will benefit from improved cash flow, with any capital investment brought forward to benefit the greater economic recovery.

Retirement Income Covenant pushed back

The retirement income covenant requires trustees to consider the retirement income needs and preferences of members. This allows for greater choice in how members take their superannuation benefits in retirement. While this was due to commence from 1 July 2020, the Government has announced it will be pushed back to 1 July 2022 to allow continued consultation and legislative drafting to take place during COVID-19. This will also allow finalisation of the measure to be informed by the Retirement Income Review.

Employment

History suggests the employment recovery following recessions can be long and arduous. It took eight years in the 1980’s to drag unemployment back to pre-recession levels of ~6% while the 1990’s took even longer. The recent experience has not been any better with unemployment in the last decade averaging well above pre-GFC levels.

Budget to drive a strong jobs recovery

Source: ABS, MWM Research, October 2020

The 2020-21 budget measures are designed to avoid this drawn out improvement with a much quicker government backed recovery via:

- JobMaker Hiring Credit of up to $200 per week will be available to employers hiring younger workers in the next 12 months. Available immediately and expected to support ~450k jobs at a cost of $4b. Importantly, the JobMaker Hiring Credit is designed to support new employment. Employers do not need to satisfy a fall in turnover test as they did with JobKeeper.

- Boosting Apprenticeships Wage Subsidy – employers will be paid a 50% wage subsidy, capped at $7k/quarter, for hiring apprentices and trainees. Available to businesses of all sizes it is expected to support up to 100k new jobs at a cost of $1.2b.

- JobTrainer fund – focus on upskilling workers with a $1b fund to support ~340k free or low-fee training places in areas of need.

Business is arguably the big winner from this budget. We expect businesses will respond with force given the range of incentives announced. Youth employment is likely to now recover quicker than expected, which should in turn help consumption, while the almost uncapped nature of the asset write-offs should see demand surge for capital equipment. While unemployment may not yet have peaked (JobKeeper yet to roll off), it is clear these measures will be very supportive for jobs growth and stimulating demand through the economy.

While the Reserve Bank of Australia (RBA) held back on policy changes at its October meeting, we note its policy settings are increasingly tied to employment. The Bank now views “addressing the high rate of unemployment as an important national priority” and “will not increase the cash rate target until progress is being made towards full employment”.

Macquarie’s economics team expects the RBA to deliver further easing at its November meeting by reducing the 3-year bond yield target and rate paid on borrowing from the Term Funding Facility from 0.25% to 0.10%. The RBA is also likely to announce purchases of 5-10 year bonds which would flatten the yield curve and less upward pressure on the A$.

We think the combined effects of monetary policy (no rate hikes till progress towards full employment) and fiscal policy (stimulatory while unemployment >6%) should prove a powerful combination in generating a jobs recovery.

Housing

The popular First Home Loan Deposit Scheme (FHLDS) will be expanded. The scheme allows first home buyers to purchase a new home with a deposit as low as 5%, without paying lenders mortgage insurance. The FHLDS has helped those with low deposits (<20%) enter the housing market while also supporting the construction industry.

The FHLDS has proved extremely popular with the first two rounds of 10,000 places (20,000 total) allocated within months. The second round of the FHLDS, which only launched on 1 July 2020, has already seen many of the approved lenders reach their full allocations.

A further 10,000 places will now be allocated for the 2020-21 financial year. The price cap will also be significantly increased which should see the scheme broaden out to new regions and postcodes.

First Home Loan Price Caps receive boost

Source: ABS, MWM Research, October 2020

Granny flats – capital gains tax (CGT) will no longer apply if building a granny flat for elderly Australians or those with disabilities. This should benefit houseowners with elderly relatives and provide further support for the construction industry.

Infrastructure

The Government will provide an additional $10b in funding towards projects over the next four years bringing total commitments for new and accelerated projects since the onset of the COVID-19 pandemic to $14b across the forward estimates. ‘Shovel-ready’ projects will be fast-tracked with funding provided for small scale road safety ($2b) and local roads and infrastructure ($1b).

Equity market implications

This was a historic budget by any measure. Most notably it marks a shift away from years of budget repair to a ‘pro-growth’ agenda. We think investors should take confidence from what is a clear plan to materially reduce unemployment from current levels, bolster the recovery via a suite of business incentives and ultimately lift the economy out of recession.

The recovery since March has strongly surprised to the upside reflecting both the extrapolation of current conditions by economists (too pessimistic) and the massive stimulus working its way through the economy. Unlike economic surprise indices in the US and Europe, which are showing clear signs of softening, Australia’s has just hit a post-GFC high. We would not be surprised if this remains an ongoing theme (data beating expectations) in the months ahead as fiscal stimulus combined with an RBA Board prepared to fully utilize the tools at its disposal.

The economy is not the equity market and this is why the market is only around 10% off its YTD highs while the economy has fallen substantially. We think this budget will go a long way towards restoring both consumer and business confidence in respect of the backstopping from government.

This does not remove the pain that is now unavoidable in respect of further consumer delinquencies, weaker spending, rising unemployment and business solvencies. However, equities don’t need strong growth to perform. They need rising profit margins alongside easy financial conditions and this backdrop does set the scene for this to eventuate – in time. We don’t think investors could have asked for much more. Certainly this was not a budget that disappointed, but the hole is deep and hence regardless of the fiscal support, it will not be a v-shaped rebound from this point forward.

Recovery to take a leg-up

Source: FactSet, MWM Research, October 2020

We highlight the major sector impacts below:Consumer

Tax cuts and welfare payments have been designed to be spent as quickly as possible and consumer-linked sectors are the obvious beneficiaries. The retail sector is already benefiting from the work from home boom and existing stimulus but the budget measures (tax cuts, asset write-offs) should support consumer spending through the Christmas period and see a broadening out of expenditure to businesses for larger items e.g. machinery, vehicles.We view domestic travel as a beneficiary from tax cuts, particularly while international borders remain closed. With retail already undergoing a massive boom for consumer durables (home offices, furniture, washing machines etc), which don’t require frequent replacing, travel is likely to provide the larger delta within the consumer sector. Significant pent-up demand, lifting of restrictions, tax relief and international border closures should all prove supportive.

Infrastructure and Building materials

The domestic building materials and infrastructure sectors should welcome a renewed focus on spending initiatives within the budget. infrastructure spending and construction. For infrastructure exposure, Macquarie analysts have a preference to Seven Group (SVW), Downer (DOW) and Monadelphous (MND) while CSR Ltd (CSR) is preferred for exposure to the detached housing cycle.

For additional budget resources you can head to the BT page here.

This article was produced in collaboration with BT and the full article can be read here.

This article was produced in collaboration with Macquarie and the full article can be read here.

Next Steps

To find out more, speak to us to get you moving in the right direction.

Important information and disclaimer

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide.

FinPeak Advisers ABN 20 412 206 738 is a Corporate Authorised Representative No. 1249766 of Aura Wealth Pty Ltd ABN 34 122 486 935 AFSL No. 458254 (a subsidiary of Spark FG ABN 15 621 553 786)