2026 Market Outlook: Expect a Bumpier Ride — But Not Necessarily a Bad One

After three strong years for diversified investors, 2026 is shaping up as a “normal” year again: positive returns are still plausible, but they’re likely to come with larger drawdowns, louder headlines, and more dispersion between winners and losers. That combination can feel uncomfortable in real time — and it’s exactly why a clear plan matters more than a perfect forecast.

AMP’s Shane Oliver sums it up neatly: 2026 should be “rough but, ultimately, ok” — with the real challenge being how investors behave when volatility arrives.

The big macro backdrop: steady growth, uneven forces

A key support for markets is that the global economy is still expected to grow at a reasonable clip. The IMF’s January 2026 update projects global growth of 3.3% in 2026 (and 3.2% in 2027), with technology investment and easing financial conditions helping offset trade-policy and geopolitical headwinds.

That “steady growth” story matters because it typically supports corporate earnings — and earnings are ultimately what share markets feed on over time. But “steady” doesn’t mean “smooth,” especially when policy uncertainty is high.

The six themes likely to drive markets in 2026

1) Interest rates are closer to the floor — but not everyone agrees where the floor is.

The US Federal Reserve’s projections (from September 2025) had the median fed funds rate at 3.4% by end-2026 (down from 3.6% end-2025), implying a lower-rate environment over time if inflation cooperates.

In Australia, the story is less settled. AMP’s base case is the RBA leaving rates on hold. But local debate has swung back toward hikes: ABC reporting in early January noted market pricing leaning to “no change” at the first 2026 meeting, but with hike expectations building later in the year.

Investor takeaway: 2026 could be a year where bonds and term deposits still “do their job,” but equity markets remain sensitive to every inflation print and central bank nuance.

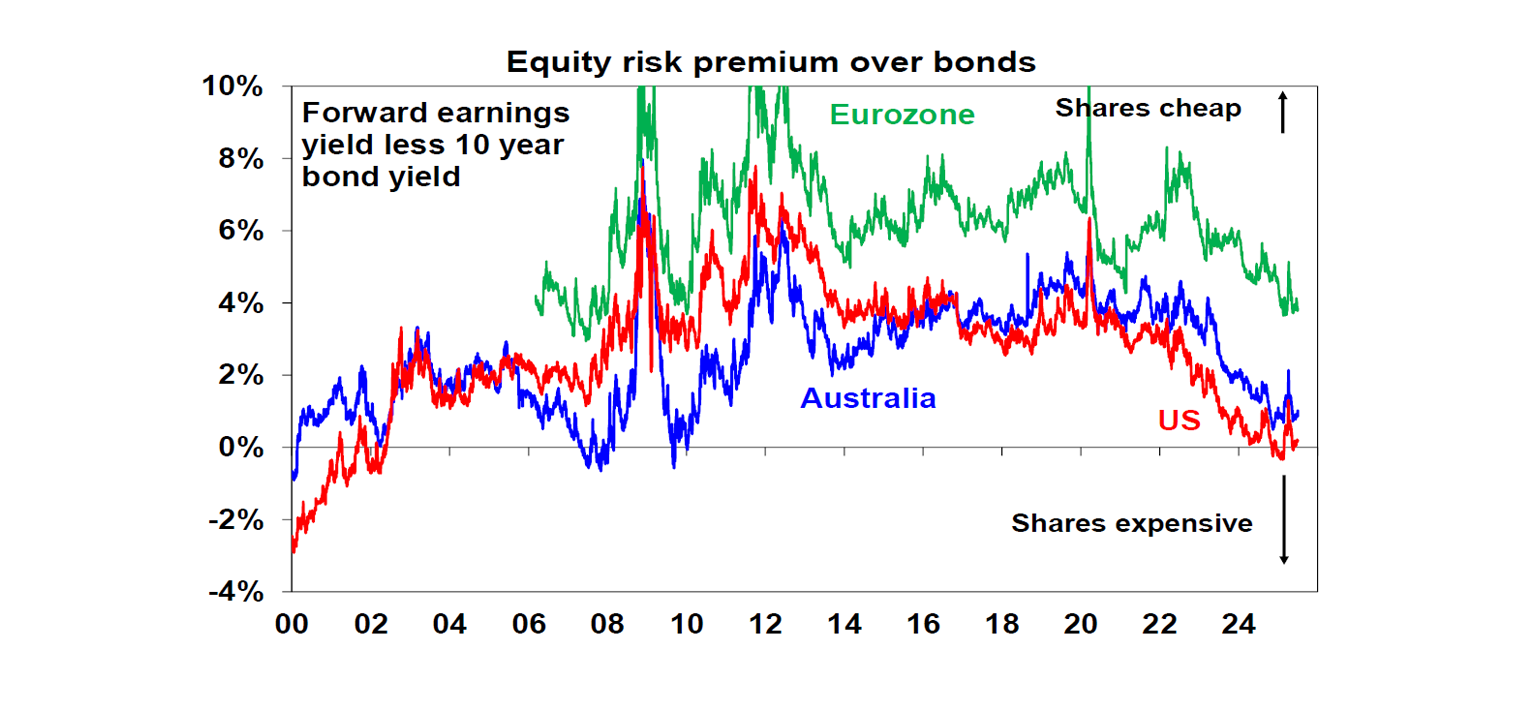

2) Valuations look stretched — which lowers the margin for error.

When markets are expensive, good news is already “in the price,” and surprises (policy, inflation, geopolitics, earnings) can hit harder. AMP flags stretched valuations and a thin equity risk premium (especially in the US), which is one reason volatility risk stays elevated.

Source: Bloomberg, AMP.

Source: Bloomberg, AMP.

3) AI remains both a tailwind and a risk.

AI-related investment has been a major market driver — but AMP also highlights the risk of “bubble-like” behaviour, including heavy capex and increasing debt funding in parts of the ecosystem.

This matters because when a single theme becomes crowded, it can create a broader market wobble even if the real economy is okay.

4) Politics and geopolitics will matter more than usual.

AMP points to US policy uncertainty and the US midterms as potential volatility catalysts, alongside ongoing geopolitical flashpoints.

This is a classic “headline risk” environment: sentiment can turn quickly, even if fundamentals haven’t changed much.

5) Australia: the consumer and housing are key swing factors.

AMP expects Australian growth to improve and profit growth to rebound, but also notes the household is still vulnerable if rates rise.

On housing, AMP’s base case is that price growth slows to ~5–7% in 2026 after a stronger 2025, reflecting affordability constraints and tighter macro-prudential settings.

6) Markets may deliver “ok” returns — but with a meaningful drawdown on the way.

A point worth stating plainly: AMP suggests another 15%+ correction is likely at some stage during 2026, even if the year finishes up overall.

That’s not a prediction of a crisis — it’s a reminder that pullbacks are normal.

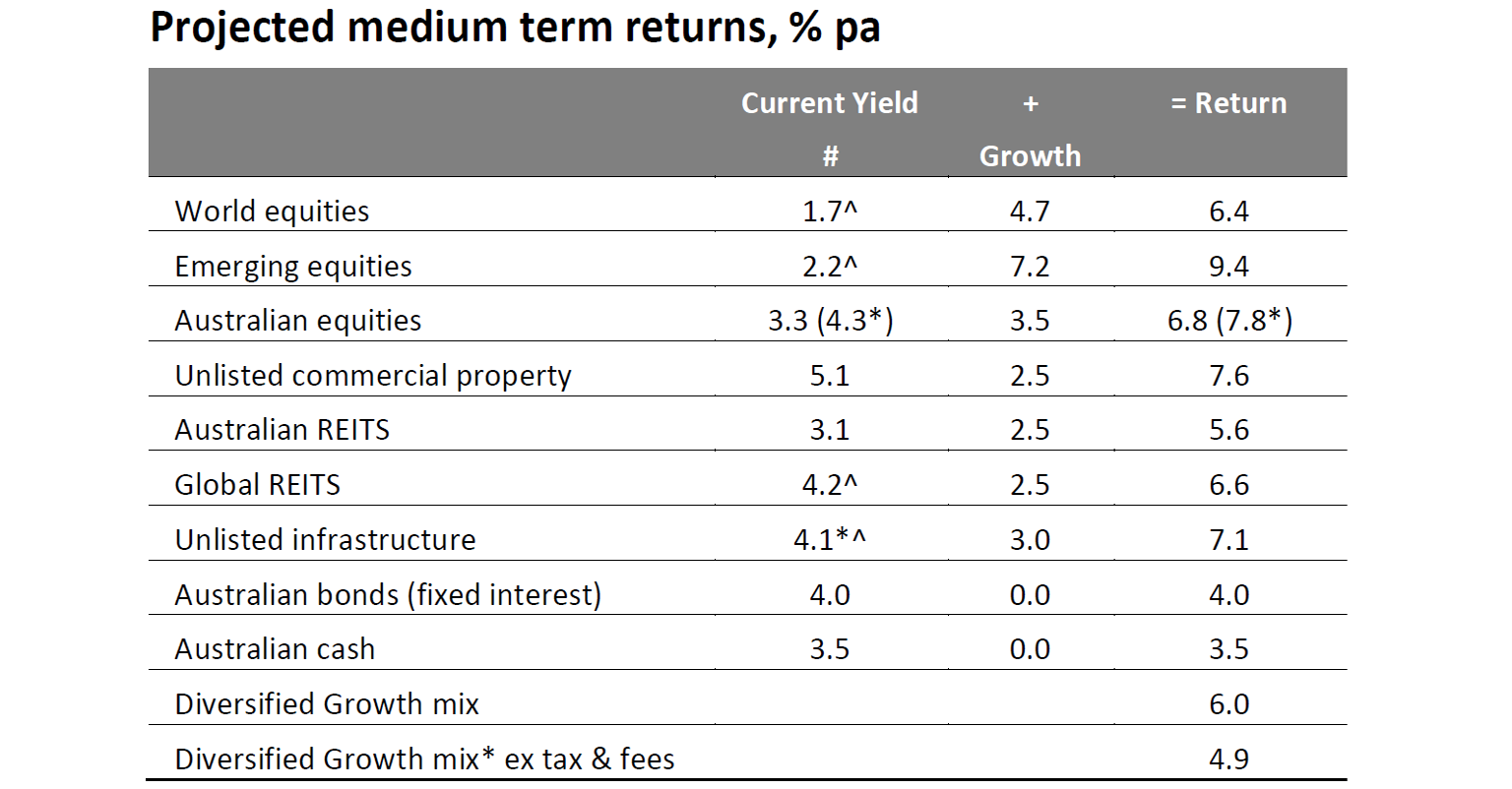

What returns might look like (and why expectations matter)

AMP’s central view is for share returns around ~8% and balanced growth super returns around ~7% in 2026, with cash returns roughly around prevailing rates (AMP references ~3.6% for cash/deposits).

This “moderate return” outlook is consistent with a broader idea many investors forget: starting yields and valuations influence future return potential.

Source: AMP.

Source: AMP.

Two practical examples for clients (because this is where the real value is)

Example 1: The 15% pullback test

Say a client has a $400,000 portfolio split roughly 70/30 growth/defensive. A 15% equity market drop might translate into, very roughly, a 7–12% portfolio drawdown depending on diversification — call it $28,000–$48,000 temporarily.

The “portfolio math” isn’t the biggest risk. The biggest risk is selling after the fall, then missing the recovery.

How to use this: set expectations early. If a client can’t tolerate that kind of temporary fall, the fix usually isn’t better market timing — it’s a better-aligned asset mix and cashflow buffer.

Example 2: Rebalancing as a simple behaviour hack

If markets fall and the portfolio drifts from 70/30 to 65/35, a disciplined rebalance forces a client to buy more growth assets when they’re cheaper — the opposite of what fear encourages. In volatile years, this single discipline can add more value than trying to outguess central banks.

Where the opportunity may be hiding in 2026

In years where the overall market return is “okay but choppy,” returns often come from being selective rather than being clever:

- Diversifying away from crowded trades (especially where valuations are most stretched).

- Income and quality in fixed income / credit (where yields can do more of the heavy lifting than in the prior decade).

- Real assets and “useful diversifiers” like infrastructure, some property segments, and (selectively) gold as a hedge when uncertainty is elevated.

The bottom line for 2026

2026 doesn’t look like a year to fear — it looks like a year to prepare for normal volatility. Global growth is expected to hold up, but investors will likely need to earn returns through discipline: diversification, rebalancing, and staying focused on long-term objectives rather than the news cycle.

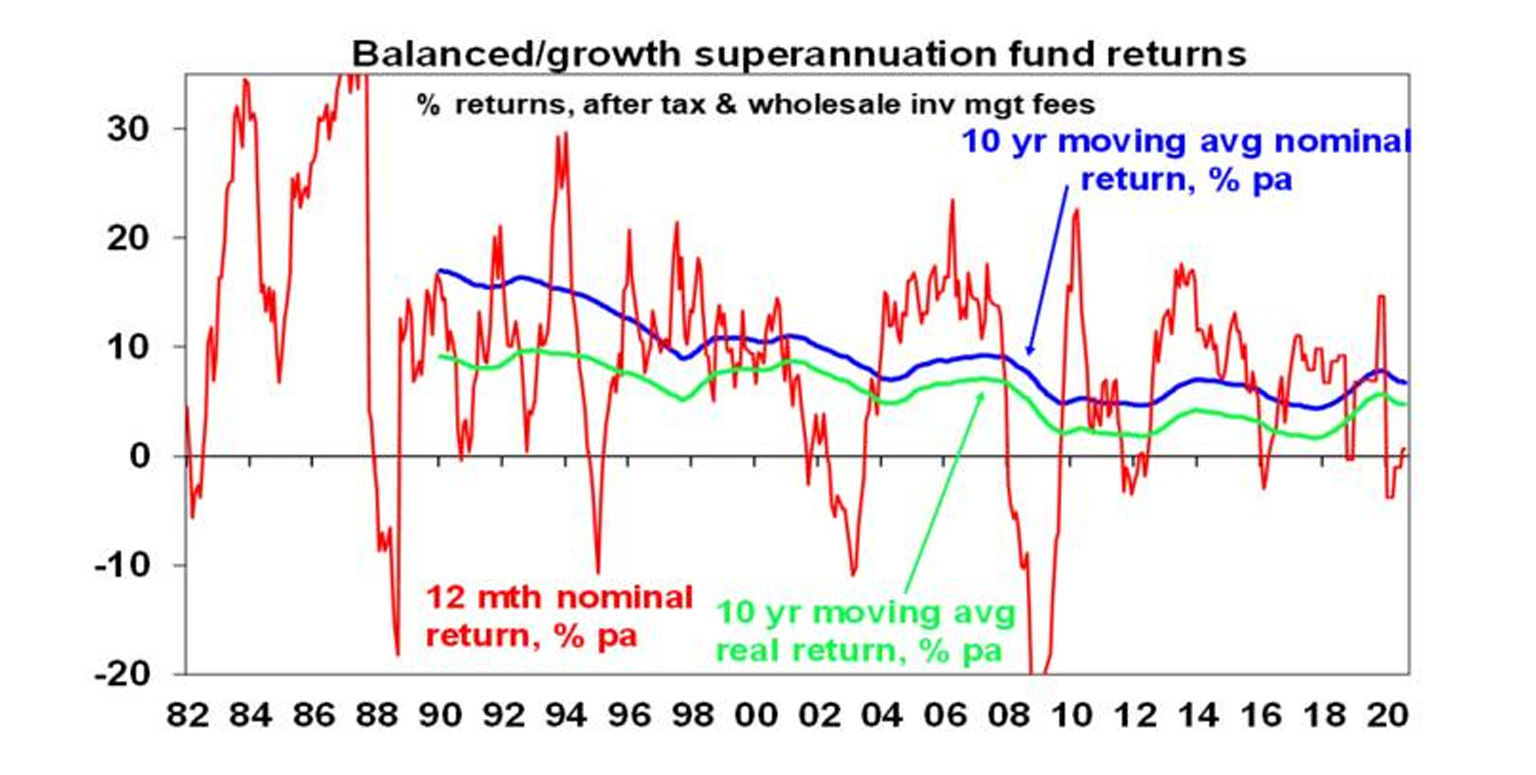

Source: Mercer/Morningstar/Chant West/AMP

Source: Mercer/Morningstar/Chant West/AMP

Next Steps

To find out more about how a financial adviser can help, speak to us to get you moving in the right direction.

Important information and disclaimer

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide.

FinPeak Advisers ABN 20 412 206 738 is a Corporate Authorised Representative No. 1249766 of Spark Advisers Australia Pty Ltd ABN 34 122 486 935 AFSL No. 458254 (a subsidiary of Spark FG ABN 15 621 553 786)