31 Mar Monthly Commentary: October 2021

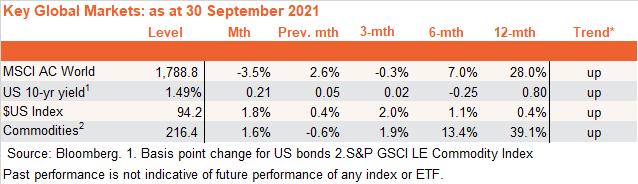

Global equities suffered a setback in September as a rebound in bond yields dragged down still lofty price-to-earnings valuations. The key market development in the month was a more hawkish than expected Federal Reserve policy meeting, which suggested a tapering in bond purchases would be announced next month and U.S. official rates could rise as early as late next year. Also, unnerving sentiment were financial difficulties with leading Chinese property developer Evergrande, and persistent signs of upward inflation pressures due to lingering supply-chain disruptions.

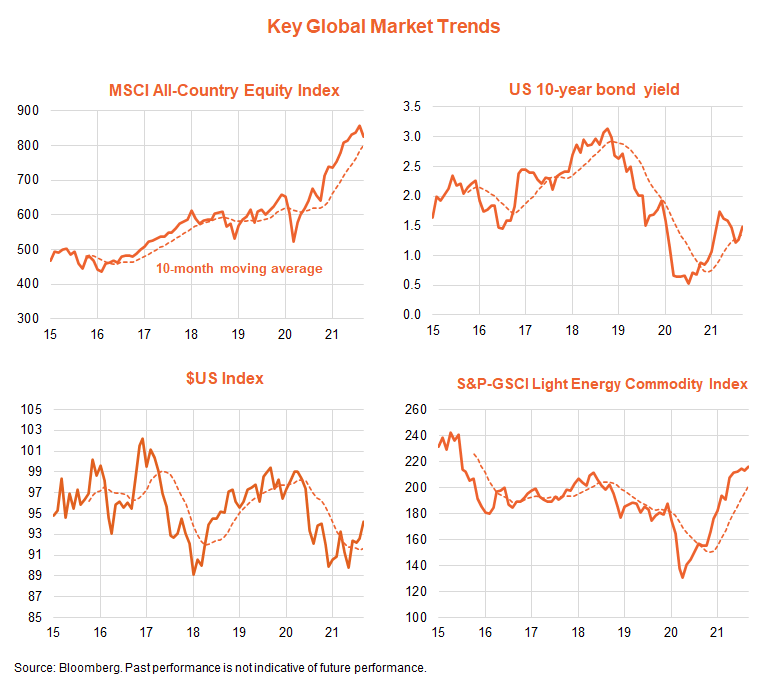

As evident in the chart set below, despite the pullback in equities, the trend in stocks remains upward. The trend in bond yields, the U.S. dollar and overall commodities also appears upward.

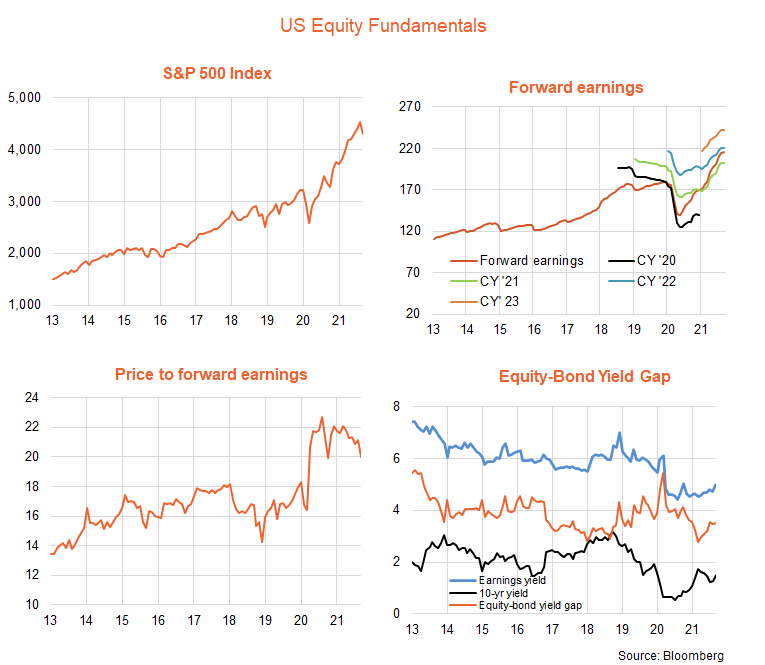

Global equity fundamentals – valuation challenges if rates rise further

The nearer-term fundamental picture for equities is mixed. As evident in the chart set below, the U.S. equity market’s uptrend in recent months has been driven by growth in corporate earnings, which are still expected to show strength over the coming year – rising by around 10-15% by end-2022 based on current market expectations.

The more challenging aspect is valuations: while the PE ratio has corrected from 22 to 20 so far this year, it remains above its range of 14 to 18 in the pre-COVID years since 2013, which in turn reflects the fact that 10-year bond yields and the equity-to-bond yield gap (EBYG) are also somewhat below their average over this period.

If bond yields rise further, there will be greater downward pressure on PE valuations, unless the EBYG holds at lower levels than that evident in recent years (indeed, it did average well below 3% in earlier decades).

For example, if U.S. 10-year bond yields rise from 1.5% to 1.75%, and the EBYG holds around the current rate of 3.5%, the PE ratio would fall to 19 (or 5% below end-September levels). If bond yields rose to 2% (my end-2022 target), with the EBYG holding steady at 3.5%, the PE ratio would need to fall to 18.2, or 9% below end-September levels.

All up, allowing for growth in earnings and some dividends, it’s still possible for U.S. equities to produce positive returns on a one-year view, though potentially in the mid-single digit growth range. That said, the one-year base case outlook for bond returns would be even lower.

Global equity themes** – potential value opportunities

The chart set below outlines trends in several key ‘thematic tilts’ across global equity markets. As evident, U.S./growth exposures suffered a relative pullback in September likely reflecting higher bond yields. More broadly, based on trends relative to their 10-month moving average, current trends still favour U.S. over non-U.S. markets, though value is now trending ahead of growth, which is also consistent with tentative signs of improvement in Australia relative to the global market. Developed markets are also still trending ahead of emerging markets.

This article was originally produced by David Bassanese from BetaShares you can read the full article here.

Next Steps

To find out more about how a financial adviser can help, speak to us to get you moving in the right direction.

Important information and disclaimer

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide.

FinPeak Advisers ABN 20 412 206 738 is a Corporate Authorised Representative No. 1249766 of Spark Advisers Australia Pty Ltd ABN 34 122 486 935 AFSL No. 458254 (a subsidiary of Spark FG ABN 15 621 553 786)

No Comments